Full size / The large tonnage of white quartz sand at Santa Maria Eterna is of superior quality with high grades of silica and exceptionally low levels of impurities. (Source)

Disseminated on behalf of Homerun Resources Inc. and Zimtu Capital Corp.

Since initiating coverage on Homerun Resources Inc. in June, the company‘s share price has more than doubled and last traded at $0.90 with a current market capitalization of $43 million. This impressive performance was backed by major announcements in July (receipt of signed Material Supply Agreement for high-purity silica sand from a district-scale, fully permitted mine in Bahia, Brazil) and August (execution of a confidentiality commitment document with Companhia Baiana de Pesquisa Mineral (CBPM) to complete due diligence and to negotiate the terms to explore and develop additional high-purity silica resources controlled by CBPM in Belmonte, Bahia, near the Port of Ilheus).

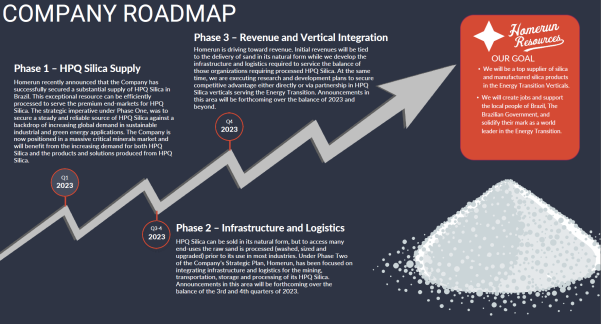

Shortly thereafter, Homerun launched a new website and published a corporate presentation disclosing highly interesting details about its silica sand supply from the Bahia Silica Sand District and that management is “working to finalize lease or ownership relationships with the two Brazilian companies“.

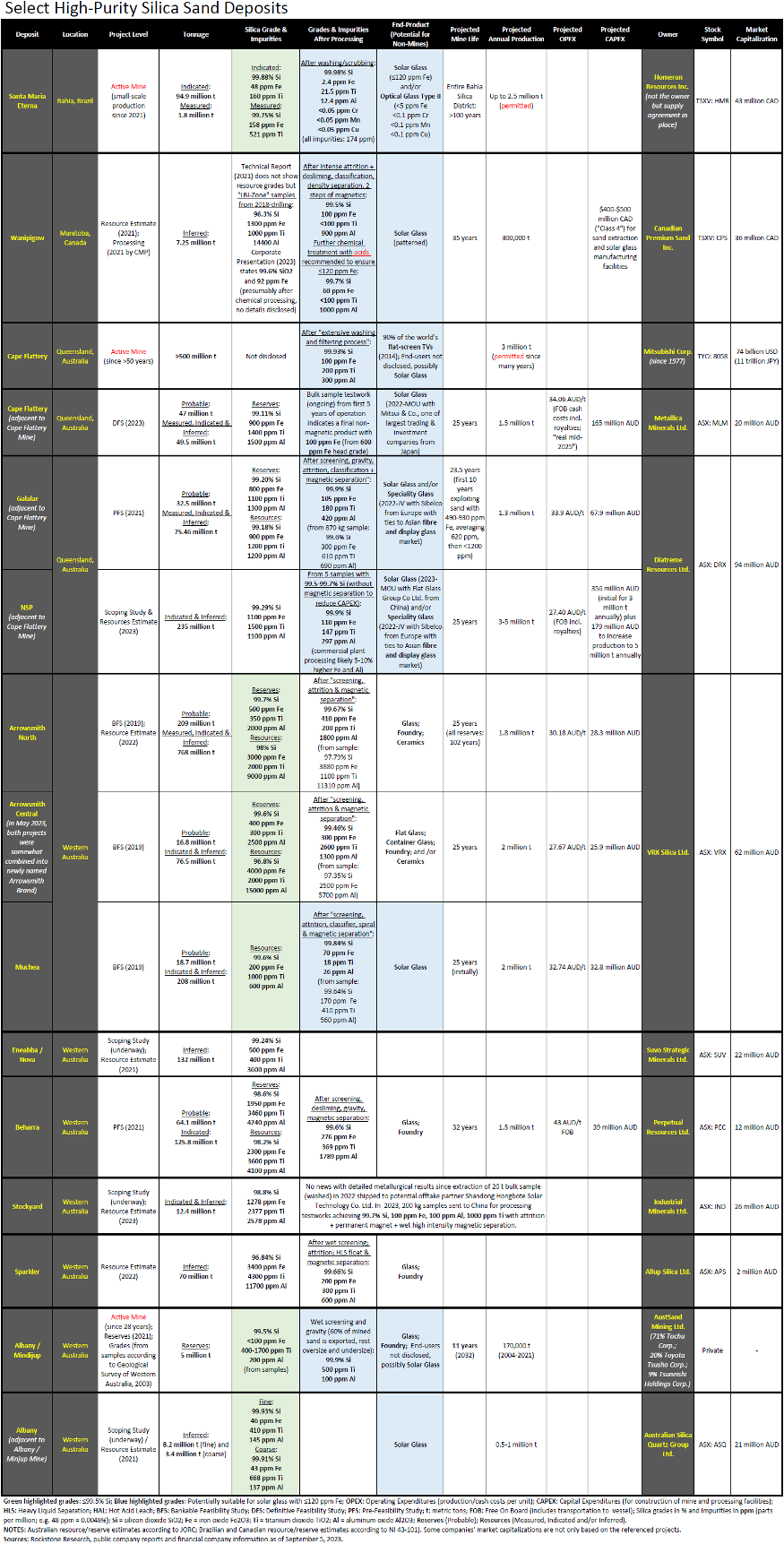

In this respect, it might be worthwile to compare the Bahia Silica Sand District (also known as the Santa Maria Eterna formation) with other producing silica sand regions and publicly listed development companies in terms of tonnage, grade, and most importantly the reduction of impurities with simple (or complex) processing methods in order to fulfill the strict specifications for the manufacture of solar glass, a strongly growing industry paying high prices and targeted by most silica sand developers. In view of all the challenges that many other silica sand projects are facing (e.g. complex metallurgy, tortuous permitting), the advantages and opportunities for Homerun come to light.

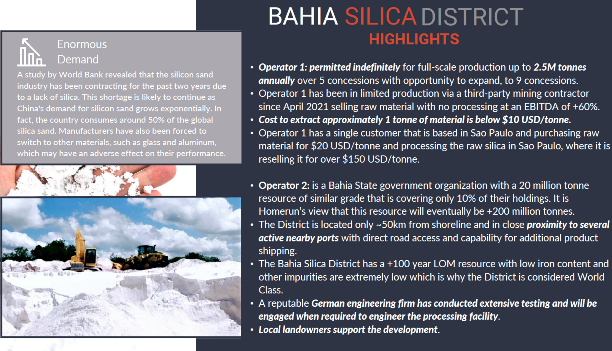

Homerun‘s latest corporate presentation not only shows pictures of the extremely white-coloured silica sand (i.e. very few impurities) at the fully permitted Santa Maria Eterna mine within the Bahia Silica District, but also states Measured & Indicated Resources totaling 96.7 million t from “Operator 1“, with whom Homerun signed a supply agreement in July. When comparing the tonnage and grades with some of the world‘s largest and highest quality silica sand mines in Australia, along with select development projects, Homerun‘s supply agreement puts the company on top of the list, especially if management succeeds in finalizing a lease or ownership relationship.

In August, Homerun announced an agreement with Bahia‘s state-owned company CBPM (“Operator 2“) who controls silica sand deposits in the same district with limited resources delineated to date (20 million t at similar grades as “Operator 1“) yet with an exploration target of >200 million t.

Full size / “Homerun has entered into an interim supply agreement with a Brazilian company for raw HPQ silica sand from its resources in the Bahia Silica Sand District in the Bahia State of Brazil. Homerun is working to finalize lease or ownership relationships with the two Brazilian companies that share ownership of the large HPQ silica resources in the District. The supply agreement is backed by a fully permitted operation with an annual allowance of up to 2.5M tonnes and an Indicated Resource of 94,894,847 tonnes with an average grade of 99.88% SiO2, 48ppm Fe, 160ppm Ti, and 102ppm Ca and a Measured Resource of 1,836,631 tonnes with an average of 99.75% SiO2, 158ppm Fe, 521ppm Ti and 93ppm Ca. This HPQ silica will be Homerun’s initial supply from the District and will be processed and shipped from port facilities located in Ilheus and / or Salvador, Bahia.“ (Source)

Full size / On August 1, 2023, the signing of a confidentiality commitment document between Homerun and CBPM was announced. From left to right: Manoel Barretto (CBPM‘s Technical Director), Henrique Carballal (CBPM‘s President), Brian Leeners (Homerun‘s CEO). About CBPM: Companhia Baiana de Pesquisa Mineral (CBPM) is the mineral research and development company of the State of Bahia, Brazil. Its activities are centered on expanding and improving geological knowledge of the Bahian territory, by identifying and researching its mineral resources and promoting their use by attracting private initiatives to this end. Founded on December 18, 1972, CBPM is recognized as one of the most dynamic companies in mineral research in Brazil. The collection of geological data and information, generated and disseminated by it has contributed to making the State of Bahia one of the best studied and geologically known Brazilian states, highlighting the great diversity of its geological environments and mineral deposits. CBPM’s stated mission is to promote the development of the mineral sector in the State of Bahia with technical, economic and social efficiency, in harmony with the preservation of the environment. (Source)

Excerpts from the article “Bahia will encourage strategic mineral projects for energy transition“ (August 21, 2023):

“Henrique Carballal, president of CBPM, said that the state wants to encourage the discovery, production and processing of minerals that will boost the energy transition that promises to revolutionize the world economy in the coming decades. In addition, invest in the creation of infrastructure and logistics... “The presence of CBPM is important to establish the necessary dialogues to find partnerships and also so that we can influence the federal government in the construction of logistics, infrastructure, because we need, in addition to discoveries, promotion so that the private sector can develop the extraction, production and processing of most of these ores in the state,” said Carballal... The Companhia Baiana de Pesquisa Mineral (CBPM) is a case of success among state-owned companies in Brazil that operate in mining. The company researches mineral resources in the territory of Bahia, encourages their economic use through partnerships with the private sector. Some examples of how this partnership works are the nickel projects, by Atlantic Nikel, in Itagiba; vanadium and titanium from Largo Resources, in Maracás, and the Canadian company Equinox, which started producing gold in the municipality of Santa Luz.“

Excerpts from the article “From the top of CBPM, Carballal promises new investments for mining in Bahia“ (August 27, 2023; freely translated from Portuguese):

“Two months into his new position as head of the Companhia Baiana de Pesquisa Mineral (CBPM), Henrique Carballal spoke about his goal to make Bahia, Brazil‘s 3rd largest mining state, an increasingly important player in the sector and an attractive destination for the establishment of factories and operations that will turn the state‘s economic machine around. “I think you‘re in for some big surprises. I can‘t divulge everything, because at CBPM we‘re executing the policy and the guiding light of this process is Governor Jerônimo, so he‘s the one who should announce it, but later this year we should have 2 factories coming to Bahia, one for cement and one for silica,“ he said and added: “[...] We also have an area of silica that will be handed over to the private sector, with a commitment to set up another factory to process this silica here in Bahia.“ In 2022, Bahia‘s commercialized mineral production grew by 7%, with a gross value of R$10.2 billion, according to data from the Brazilian Mining Institute (IBRAM). The sector has more than 14,000 direct jobs and around 150,000 more indirect jobs. According to Carballal, “Bahia will be the next big thing in mining. The mineral production that Bahia will grow even more is linked to minerals that are fundamental to the energy transition. We need to ensure that this mineral exploitation takes place while respecting the environment and fundamental social policies, but we also need to understand that Bahia cannot miss out on this opportunity. We are in a position to attract large industries here and supply the thirst that the world market will have for everything linked to the energy transition.“

Excerpts from the article “Municipal Government promotes mining opportunity and economic boost in Santa Maria Eterna – Belmonte“ (2021; freely translated from Portuguese):

“The municipality [of Belmonte in Bahia] seeks partnerships with the State Government and the private sector to generate new business opportunities and offer jobs and income to the community of Santa Maria Eterna... Studies by the Secretary of Industry, Commerce and Mining of the State of Bahia, indicate that Santa Maria Eterna is privileged with high purity silica sand, as it has rigorous specifications to lend itself to the manufacture of transparent flat glass and special glass, which can generate, as a by-product, fine sand applicable in the ceramic industry (white and glazed ceramics). The silica sand from Santa Maria Eterna can also be used in the production of sodium silicate and in the production of silicon tetrachloride and its derivatives. With economic compensation, even purer sands can be obtained by magnetic separation and/or acid leaching.“

Full size / The picture shows initial, small-scale mining activity at the Santa Maria Eterna deposit within the Bahia Silica District. Studies indicate that the district is priviliged with high-purity silica sand and one of the world‘s lowest impurity levels, which can be reduced further with processing as below table indicates. (Source)

Full size / PDF-Version / Note that silica sand grades and mineralization described in similar deposits on other properties are not representative of the mineralization on Homerun‘s or its partner’s properties, and historical work and activities on its properties have not been verified and should not be relied upon.

The above table compares Homerun‘s supply agreement (Santa Maria Eterna mine in Bahia, Brazil) with other active mines and select publicly traded companies‘ high-purity silica sand projects. With 99.88% SiO2, Santa Maria Eterna has the second-highest silica grade of all referenced projects (after Australian Silica Quartz Group Ltd.‘s Albany deposit in Western Australia with 99.93%), however hosting a much larger resource (96.7 million t) than Albany (11.6 million t). In regards to the most crucial impurity (iron oxide), Albany (46 ppm Fe2O3) has a bit lower level in its resources than Santa Maria Eterna (48 ppm). Most importantly, none of the referenced projects has demonstrated to reduce the iron impurity as low as Santa Maria Eterna (2.4 ppm), whereas this feat is accomplished with simple washing/scrubbing. Most other projects have great difficulty in reducing the iron impurity to meet the strict specifications of solar glass (≤70 ppm Fe2O3; some other sources state 120 ppm as maximum), that is to say even with extensive physical or even chemical processing methods resulting in high upfront capital costs (CAPEX) to built such complex processing plants.

The table reveals that the Santa Maria Eterna deposit is exceptional in terms of hosting large resources with very low impurities. On top of that, the advantage of Santa Maria Eterna being a permitted mine (up to 2.5 million t annually) can not be understated as Australian projects have shown that permitting is a lengthy and cumbersome process with an uncertain outcome, resulting in relatively low market capitalizations despite supply agreements in place (or in sight) as off-takers scramble to lock in any potential future supply despite metallurgical and/or permitting challenges.

BRAZIL

Santa Maria Eterna

Full size / Image of the sand outcropping (upper part of the photo) at the Santa Maria Eterna silica deposit. (Source)

Excerpts from “Quartz sand resources in the Santa Maria Eterna formation, Bahia, Brazil: A geochemical and morphological study“ (2015):

High purity quartz has been an essential raw material for several industrial applications, such as the production of silica glass, a key material for high-end products, for example UV-lamps for purifying water, poly- and monocrystalline silicon solar cells, through its use as material crucibles and special devices with low thermal expansion. To be turned into a good quality silica glass, the quartz raw material must have unique characteristics. It must be pure, containing only traces of metallic impurities such as Al, Fe, and Ti, which can severely compromise the silica glass‘ quality, jeopardizing its applications.

Regarding the manufacturing of crucibles, all excess [impurities] can generate brown spots in the glass when it is in contact with the silicon melt and produce devitrification, reducing the device‘s lifetime. Additionally, Fe, Ti, and other metallic impurities can contaminate the silicon melt. In the case of lenses and tubes, chemical pollutants can significantly affect the transmittance, especially in the ultraviolet range. Quartz for silica glass production must also contain low amounts of fluid inclusions. Such inclusions can produce bubbles during the fusion of the raw material into silica glass. Usually, the amount of fluid inclusions in quartz is related to its opacity, which can be used to grade the samples to obtain better material quality.

Quartz resources with such characteristics are rare and their exploitation and processing are very costly. Often, companies start from less pure raw materials and use industrial processing to achieve the desired chemical purity. Such processing commonly involve acid leaching using HF and other hazardous materials. The higher the amount of impurities in the raw material, the more expensive and environmentally damaging is the purifying process. Some chemical impurities, as Al, Ti and Ge, substitute Si atoms in the quartz lattice and are much harder to be removed than Na, Ca and K that are often located in fluid inclusions. As a result, the chemical composition of the raw material, that is, the abundance and characteristics of its impurities, is a key factor in determining the economic potential of the quartz resource.

Brazil hosts many different kinds of quartz resources, many of them with a high degree of purity and favorable technological characteristics for silica glass production. However, most of the mines ascribed with high chemical purity, are rocky quartz deposits, but there are a number of quartz sand deposits as well. Most quartz sand deposits explored in the country are located in south and southeastern Brazil and are widely used by float glass manufacturers.

In this study, a newly discovered quartz sand deposit of economic potential, located in the state of Bahia, northeast Brazil, is described. Samples from the deposit were characterized by Inductively Coupled Plasma Mass Spectrometry (ICP-MS), fluid inclusion analysis, Scanning Electron Microscopy (SEM), cathodoluminescence and fusion over silica plate to document the chemical and physical properties of the raw material. This information were analyzed in order to evaluate whether or not the sand is fit for producing silica glass and to better understand its geological history.

Full size / Overall aspect of the sand. (A) shows the material as it is in nature, as gravel, and (B) shows the gravel in a low magnification photograph. (Santos et al., 2015; Source)

The deposit is located in a geological formation called Formaçao Santa Maria Eterna, in the south of the Bahia State, Brazil... The Santa Maria Eterna formation is situated southwest to the city of Belmonte. The formation crops out in an area of approximately 30 times 20 km... The mine is located in the central part of the area. The formation consists almost exclusively of quartz sand and minor quantities of quartz pebbles up to 20 cm... It is generally accepted that both the Serra do Paraíso and the Santa Maria Eterna formations were deposited over the Panelinha conglomerate in a marine environment... The deposit itself is not being commercially exploited [as of 2015]. There are, however, projects for using the sand in the manufacture of special glasses and mining activities may start within the next few years.

The economic viability of the quartz sand deposit of Santa Maria Eterna formation as raw material to produce silica glass depends on its chemical composition and propensity to form bubbles... The comparison of quartz from Santa Maria Eterna to other sources of high purity quartz described in literature, shows that the studied sand has a very low Al content as it is found in nature... Al is stated as the most difficult element to remove, because it substitutes Si in the crystalline structure... Overall, the chemical composition of the sand in the Santa Maria Eterna formation makes it a valuable resource. Probably it could be purified to become a commercial high purity quartz source to produce a good and clean transparent glass. Nevertheless, the studied material can be used as a raw material in the silica glass industry to obtain opaque crucibles without the proposed treatments.

Conclusion: The high purity quartz sand of Santa Maria Eterna formation is a promising ore resource. It was probably formed by silica precipitation from a marine environment, generating an ore with very low Al and high Mg and Ca contents, contained mostly in mineral inclusion. Very few accessory minerals (other than mineral inclusions) are found in the deposit and it is also remarkably homogeneous. Its viability as raw material for silica glass production showed adequacy for several applications. The quartz sand is sufficiently pure and the product of fusion has little number of bubbles. Moreover, as the main impurities are in fluid and mineral inclusions, they could be removed by purification. The resulting powder could become a competitive product in the high purity quartz market.

Full size / Geological map of the Santa Maria Eterna region (Moreira, 2005; Source)

The Santa Maria Eterna silica sand deposit is immediate to the south of the town Santa Maria Eterna, located 59 km southwest of Canavieiras, in the southern region of Bahia. Road access from Salvador, the capital of Bahia, can be done on a route of approximately 586 km on paved roads.

The Port of Ilhéus (pictured below) is located 115 km north of Canavieiras. It‘s also a medium-sized port, whereas the maximum length of the vessels recorded to having entered this port is 334 m (same as Port of Salvador). From Santa Maria Eterna, it takes about 3 hours by car (197 km) to reach Ilhéus. Recently in July, the construction of a major railroad project was started, connecting the mines in Bahia to the Port of Ilhéus. The first 126 km of railway should be ready in 36 months. The Port of Ilhéus, today the main grain exporter in Bahia, has a handling capacity of 1 million tons of cargo per year, and has emerged in the tourism segment, receiving a considerable volume of cruise ships each year in season periods. The Port of Ilhéus has its history linked to the rich cocoa history of Bahia (see here). Today, in addition to cocoa, its cargo handling list includes soy, corn, almonds, magnesium oxide, nickel concentrate, industrialized parts and general cargo.

The Port of Salvador is a medium-sized port handling over 3 million tons of cargo in 2007. In recent years, the Port of Salvador has received substantial investments in its infrastructure. The maximum length of the vessels recorded to having entered this port is 334 m. A road distance of about 59 km is between Santa Maria Eterna and the Port of Canavieiras, a medium-sized port. The maximum length of the vessels recorded to having entered this port is 12 m. The Port of Belmonte is also a medium-sized port, whereas the maximum length of the vessels recorded to having entered this port is 34 meters. The road distance from Santa Maria Eterna to Belmonte is about 157 km.

“According to data from the National Mining Agency (ANM), Bahia was the state that invested the most in mineral research from 2019 to 2021. In total, over R$ 1.16 billion [currently $233 million USD] were invested in public and private investments, covering the stages of research authorization and mining operations. Over the period from 2010 to 2021, investments exceeded the mark of R$ 2.3 billion, which has contributed significantly to the success of the mining industry in Bahia.“ (“CBPM Announces Discovery of the Metallogenic Province in Northern Bahia“, 2023)

“Between 2022 and 2025, Bahia will receive a total of 70bn reais [currently $14 billion USD] in investments in the mining sector.“ (“How Brazil‘s Bahia state is becoming a mining hub“, 2022)

As per Homerun‘s news-release on July 22, 2023: “[...] the Company completed a significant milestone in its business development plan with the receipt of the signed Material Supply Agreement between Homerun Resources Inc. (“HMR”) and the vendor (“Vendor”) detailing the operational terms regarding the supply of high purity silica sand sourced from the Vendor’s district-scale, fully permitted project in Bahia, Brazil. Under the Agreement, the purchase price has been set at US$20.00 per tonne, net of Homerun’s obligation to cover recoverable costs and applicable taxes. The applicable taxes in Brazil are dependent on customer jurisdiction both domestically and for international shipments. Recoverable costs are dependent on whether the mode of operation is service contractor or internal capital equipment or equipment lease. This is yet to be determined.“

AUSTRALIA

Australia has the highest number of publicly traded companies focused on high-purity silica sand projects, either located in Queensland or Western Australia. The Australian Government has recognized the importance of silica sand in its Austrade Critical Minerals Prospectus 2022, however virtually all projects are looking at offtakes for Asian markets.

Queensland

Cape Flattery Silica Mines (CFSM) has been producing silica sand since 1967 and was purchased by Mitsubishi Corp. in 1977, bringing a deep water jetty into operation in 1987. Today, the mine employs over 80 people, according to its website, which also touts CFSM having “the highest production of silica sand for any mine in the world“ along with “the best silica in an unbeatable location“. With an annual production of >3 million t, CFSM is “the largest global exporter of silica sand and has the highest production of silica sand for any mine in the world“, according to AREEA. The mine site lies directly on the east coast of the Cape York Peninsula and abutts the World Heritage listed Great Barrier Reef Marine Park. The mining leases cover land owned by the traditional owners of the Yuuru Peoples (consisting of the Dingaal, Nguurruumungu and Thanil clan groups), which means that “mining cannot commence until approval from the traditional owners, environmental license obtained from the Queensland Government, flora and fauna survey and a drilling survey of dunes completed“. The large leased-property (63 km2) has “significant untapped resources of silica sand“, estimated at >500 million t with grades as good as 99.93% SiO2, 100 ppm Fe, 200 ppm Ti and 300 ppm Al (after an extensive washing and filtering process on site). The company‘s CFO, Samat Narula, said in 2014, when the mine site and jetty was damaged by a cyclone: “We are sort of the quiet achievers and we are the biggest silica mine in the world. And 90 per cent of the world‘s flat screen TVs have Cape Flattery silica sand in them.“ CFSM also provides the silica sand used in many of the world‘s iPhone and Android phone screens.

Full size / Cape Flattery Silica Mines: Mitsubishi not only owns one of the world‘s largest silica sand deposits but also one of the highest quality sands with impurities reduced on-site with an extensive washing and filtering process, whereafter the graded sand is sent to the near-by wharf for loading and export to Japan and other parts of Asia. (Source)

Adjacent to CFSM, Diatreme Resources Ltd. is developing its Galalar and NSP projects. While metallurgical testing of sand from Galalar has demonstrated a reduction of iron impurities to 105 ppm without acid, some few initial samples from NSP showed that iron can be reduced to 110 ppm without acid but that commercial processing would likely result in 5-10% higher levels of iron and aluminum. CEO Neil McIntyre said in 2022: “Traditionally, a lot of the silica market in Australia has been dominated by trading houses – Japanese trading houses, in particular. Mitsubishi is one of them and there are two or three others out of Western Australia that dominate that market. This creates a market that’s incredibly opaque and you can’t easily see the substance behind it in terms of pricing and in terms of the products they’re producing. So what we’re seeing is a level of maturity coming into the silica market now, with a number of listed companies like us. There’s about three or four in Western Australia. We’re a public company, we publish and talk about everything to do with our business, and that’s new.” Diatreme inked a joint venture agreement with global industrial minerals company Sibelco in 2022 and recently signed a non-definitive MOU with Flat Glass Group Co. Ltd. from China. Diatreme‘s deposits are in a remote region, close to the surface with only a limited vegetation and topsoil covering. The average thickness of the sand within Galalar‘s reserve pit shell is 12 m, however several interburden layers with high iron impurities are designated as waste. The projects re located within the Cape Flattery Port area – owned and operated by Ports North, a Queensland Government-controlled corporation. Ports North is the owner of the jetty leased by Mitsubishi, whereas the ship-loading equipment on the jetty is primarily owned by Mitsubishi.

CFSM‘s and Diatreme‘s neighbor is Metallica Minerals Ltd. In it‘s November-2022 presentation, the company states that “Environmental management at the Cape Flattery Silica project will be comprehensive“ and proudly states that “no chemicals will be used in production“ (the company has been waiting on environmental and land ownership agreements for years). Metallica reassures that HAL (hot acid-leaching) will not be undertaken on-site – but has to be done off-site by some prospective purchasers of its sand as preliminery results of metallurgical testwork demonstrate that acid is needed to reduce iron impurities below 120 ppm (in order to meet requirements for solar glass). The company admits that more metallurgical testwork is needed to confirm process pathways to reduce iron content to less than 120 ppm, which is planned to be incorporated into the DFS metallurgical program. To reach the silica sand layer, removal of 50 cm topsoil is needed. using a dozer or grader. Thereafter, silica sand extraction can commence with direct loading from the working face by a wheel loader, loading silica sand into a mobile feeder unit. Quality control processes must be employed at the working face to maintain quality of the feed into the processing plant (due to areas of poorer quality silica sand expected to be encountered). Water is added to the silica sand passing through the mobile feeders and the slurry is pumped to the processing plant. The Wet Concentration Plant (WCP) is designed to refine the sand to reduce heavy minerals. Metallica names the risks of its proposed mining and processing project, such as “Environmental and social licences to operate, including delays to project approvals. Additionally, increased output from existing and new producers and projects currently progressing through project development and approvals programs may present a market risk. The Company will continue formal negotiations with the Traditional Landowners (Hopevale Congress Aboriginal Corporation as agent for the Nguurruumungu Clan, and Walmbaar Aboriginal Corporation as agent for the Dingaal Clan).“

Western Australia

Western Australia hosts significantly more silica sand projects than Queensland. Moreover, most silica sand deposits in Western Australia have less iron impurities than the raw sand in Queensland. However, when looking at metallurgical testworks completed, some major projects in Western Australia have more difficulties in reducing iron impurities below 120 ppm. Only sand from Muchea (VRX Silica Ltd.) achieves the feat of reducing iron contaminants to 70 ppm, making its processed sand suitable for solar glass without having to use acid during on-site processing. Note that the Albany mine (AustSand Mining Ltd.) and the adjacent Albany deposit (Australian Silica Quartz Group Ltd.) host raw silica sand with less than 100 ppm and 46 ppm iron, respectively, albeit both deposits are rather small with 5 million t reserves and 11.6 million t resources, respectively.

Interestingly, projected CAPEX for on-site processing facilities are much lower for projects in Western Australia (averaging 31.5 million AUD among 4 projects for an annual production averaging 1.8 million t) than in Queensland (averaging $196 million AUD among 3 projects for an annual production averaging 1.9 million t).

CANADA

Silica sand deposits occur throughout Canada, with active mines mostly in Ontario (by far Canada‘s largest sand and gravel producer), Alberta and Quebec. In western Labrador, large tonnage quartzite (hard-rock) deposits can be found (e.g. 17 samples averaged 571 ppm Fe, 12 ppm Ti, 311 ppm Al, 690 ppm CaO). Manitoba used to be a significant silica sand producer as the Winnipeg Formation contains the largest known deposits of silica sand in the province. Historical quarrying of outcropping silica sand deposits at Black Island on Lake Winnipeg started in the 1920s and stopped in the 1980s, causing environmental damage until today. The high impurities in the “high-purity“ silica sands (i.e. iron, aluminium and titanium in the 1000s ppm) contributed to severe acid-mine drainage with toxic heavy minerals being released into the groundwater and into Lake Winnipeg. It was mainly the oxidation of pyrite in the shale layer above the sand contributing to the environmental damage (aquifer contamination) caused by historic quarrying. After almost 100 years of leaching, acidic hematite (reddish-brown) coloured water is still running out of abandoned Black Island quarry pits today. At the height of its operation (1960-1980s), roughly 10,000 t of silica sand was mined annually at Black Island. Just a few kilometres from the historic Black Island pits, Canadian Premium Sand Inc. hopes to mine 1.3 million t of silica sand annually for possibly 50 years from its Wanipigow deposit. It was previously defined as a frac sand resource as part of a PFS (2020). Presently, CPS proposes to assess and develop “a high-grade (high silica, low iron) portion“ of the open-pitable deposit for use in the glass manufacturing industry. Specifically, CPS is in search of investors willing to finance an on-site sand processing facility and an off-site solar glass manufacturing plant for $400-500 million. The deposit is located along the east shore of Lake Winnipeg and adjacent to the Hollow Water First Nation‘s reserve lands. The proposed mining project received public opposition in 2022 in regards to “putting drinking water at risk“ while “creating environmental and cultural damage“.

Full size / Abandoned silica sand mine at Black Island, Manitoba, where historic mining is still causing environmental damage due to acid drainage from the Winnipeg Formation and the overlying Black Island Member; the latter may include a pyrite (iron) rich shale, a major contributor of heavy minerals released into the water. (Source)

Click above player or here to watch drone footage of an abandoned silica sand mine at Black Island, showing severe acid drainage into Lake Winnipeg.

Sio Silica Inc., a private company based in Calgary, is proposing to extract silica sand near Vivian, Manitoba, by injecting air into the Winnipeg Sandstone aquifer to bring up a mixture of water and sand from the water table, which extends under a large swath of southeastern Manitoba and serves 8 municipalities. The Vivian Silica Project received public opposition not only in 2020 and 2021, when the extracted and on-site-processed sand was proposed for the fracking industry. Public opposition for the project remained high in 2023, despite the company having changed its name a year earlier (formerly CanWhite Sands Corp.) and switching the sand‘s destination to “green energy and technology markets“, with its website touting “solar panels, computer chips and batteries, fibre optics and speciality medical glass“ without mentioning impurity levels of its raw or processed sand.

UNITED STATES

In 2022, industrial sand and gravel production in the US was estimated at 97 million t, valued at $5.7 billion USD (averaging $58 USD/t), according to the USGS. The leading production states were, in descending order: Texas, Wisconsin, Illinois, Louisiana, Missouri, Oklahoma, Arkansas, Alabama, California, and Tennessee. Approximately 75% of the tonnage was used as frac sand and well-packing and cementing sand; and 10% as glassmaking sand. Other common uses were, in decreasing quantity of use, foundry sand, whole grain fillers for building products, filtration sand, and recreational sand, which accounted for 9%, combined. Other minor uses were, in decreasing quantity of use, chemicals, abrasives, roofing granules, silicon and ferrosilicon, ceramics, fillers, filtration gravel, traction, and metallurgic flux, which accounted for 3%, combined. The US also imports sand and gravel (estimated at 350,000 t), mainly from Canada (87%), but also from Vietnam (3%), Brazil (2%) and others (8%). An estimated 6.4 million t were exported in 2022, shipping to almost every region of the world. With 97 million t mined in 2022, the US was the world‘s largest producer and consumer of industrial sand and gravel, followed by China (88 million t) and the Netherlands (54 million t), whereas estimated world production stood at 380 million t. Of the 122 companies that produced industrial sand and gravel in the US in 2022 (from 201 operations in 32 states), one of the largest is U.S. Silica Company. The privately held company owns and operates processing plants along with silica hard-rock and sand mines in Missouri, Illinois. Michigan, Wisconsin, Pennsylvania, Oklahoma, Louisiana and Texas, most of which supply raw and processed silica sand for the oil and gas industry as well as for the construction, chemical, ceramics, foundry, glass and recreational industries.

As an exception, the Spruce Pine Mining District in North Carolina‘s Appalachian Mountains is “the source of the purest natural quartz ever found on Earth“. The Spruce Pine quartz is needed to make the fused‑quartz crucibles in which computer‑chip‑grade polysilicon is melted. In fact, there’s an excellent chance the chip that makes your laptop or cell phone work was made using quartz from this obscure Appalachian backwater. “A fire in 2008 at one of the main quartz facilities in Spruce Pine for a time all but shut off the supply of high‑purity quartz to the world market, sending shivers through the industry. Today one company dominates production of Spruce Pine quartz. Unimin, an outfit founded in 1970, has gradually bought up Spruce Pine area mines and bought out competitors, until today the company’s North Carolina quartz operations supply most of the world’s high‑ and ultra‑high‑purity quartz. (Unimin itself is now a division of a Belgian mining conglomerate, Sibelco.) In recent years, another company, the imaginatively titled Quartz Corp. has managed to grab a small share of the Spruce Pine market. There are a very few other places around the world producing high‑purity quartz, and many other places where companies are looking hard for more. But Unimin controls the bulk of the trade... Only Unimin knows exactly how much Spruce Pine quartz is produced, because it doesn’t publish any production figures. It is an organization famously big on secrecy... Unimin sells this ultra‑high‑purity quartz sand to companies like General Electric, which melts it, spins it, and fuses it into what looks like a salad bowl made of milky glass: the crucible. It’s safe to say the vast majority of those crucibles are made from Spruce Pine quartz... The quartz for the crucibles, like the silicon they will produce, needs to be almost absolutely pure, purged as thoroughly as possible of other elements. Spruce Pine quartz is highly pure to begin with, and purer still after being put through several rounds of froth flotation. But some of the grains may still have [...] interstitial crystalline contamination – molecules of other minerals attached to the quartz molecules. That’s frustratingly common. Some Spruce Pine quartz is flawed in this way... The very best Spruce Pine quartz, however, has an open crystalline structure, which means that hydrofluoric acid can be injected right into the crystal molecules to dissolve any lingering traces of feldspar or iron, taking the purity up another notch... The polysilicon is placed in those quartz crucibles, melted down, and set spinning. Then a silicon seed crystal about the size of a pencil is lowered into it, spinning in the opposite direction. The seed crystal is slowly withdrawn, pulling behind it what is now a single giant silicon crystal. These dark, shiny crystals, weighing about 220 pounds, are called ingots. The ingots are sliced into thin wafers. Some are sold to solar cell manufacturers. Ingots of the highest purity are polished to mirror smoothness and sold to a chipmaker like Intel... The wafers are then cut into tiny, unbelievably thin quadrangular chips – computer chips, the brains inside your mobile phone or laptop. The whole process requires hundreds of precise, carefully controlled steps. The chip that results is easily one of the most complicated man‑made objects on Earth, yet made with the most common stuff on Earth: humble sand.“ (Source: “The Ultra-Pure, Super-Secret Sand That Makes Your Phone Possible“, 2018)

“Brazil’s solar energy industry is set to get a boost from a government plan to have local industry manufacture inputs for the sector... “Most of our inputs today come from China, having local production can help the entire sector, including to reduce costs,“ Túlio Fonseca, CEO of solar power franchisor Energy Brasil, told BNamericas. As part of the government‘s efforts to stimulate the local industry, funding will be made available for projects through the country’s climate fund, which is managed by development bank BNDES. Solar makes up 15% Brazil’s energy matrix and is the second largest energy source after hydroelectric plants, with the expectation to reach 50% by 2050, according to local PV solar association Absolar.“ (Source)

“In a recent article titled “Could sand be the next lithium?” the Washington Post dug into the issue and found that natural batteries have significant advantages over traditional batteries... In batteries where sand is heated to upwards of 1,000 degrees Fahrenheit, the sand can hold on to that energy for a long time, with temperatures remaining over 200 degrees even when the battery’s energy is running low. The sand can hold onto the power for weeks or months at a time – a clear advantage over the lithium-ion battery, the giant of today’s battery market, which usually can hold energy for only a number of hours. Plus, the technology doesn’t hinge on supply chains and materials dominated by China – another problem faced by lithium-ion batteries.“ (Source)

Company Details

Homerun Resources Inc.

#2110 - 650 West Georgia Street

Vancouver, BC, V6B 4N7 Canada

Phone: +1 844 727 5631

Email: info@homerunresources.com

www.homerunresources.com

ISIN: CA43758P1080 / CUSIP: 43758P

Shares Issued & Outstanding: 47,504,525

Canadian Symbol (TSX.V): HMR

Current Price: $0.90 CAD (09/05/2023)

Market Capitalization: $43 Million CAD

German Ticker / WKN: 5ZE / A3CYRW

Current Price: €0.605 EUR (09/06/2023)

Market Capitalization: €29 Million EUR

Contact:

www.rockstone-research.com

Disclaimer: This report, the video interviews and the referenced news-releases contain forward-looking information or forward-looking statements (collectively "forward-looking information") within the meaning of applicable securities laws. Forward-looking information is typically identified by words such as: "believe", "expect", "anticipate", "intend", "estimate", "potentially" and similar expressions, or are those, which, by their nature, refer to future events. Rockstone Research, Homerun Resources Inc. and Zimtu Capital Corp. caution investors that any forward-looking information provided herein is not a guarantee of future results or performance, and that actual results may differ materially from those in forward-looking information as a result of various factors. The reader is referred to Homerun Resources Inc.´s public filings for a more complete discussion of such risk factors and their potential effects which may be accessed through its profile on SEDAR at www.sedar.com. Please read the full disclaimer within the full research report as a PDF (here) as fundamental risks and conflicts of interest exist. The author, Stephan Bogner, owns an equity position in Homerun Resources Inc., and also owns equity of Zimtu Capital Corp., and thus will profit from volume and price appreciation of those stocks. The author is being paid by Zimtu Capital Corp. for the preparation, publication and distribution of this report, whereas Zimtu Capital Corp. also holds an equity position in Homerun Resources Inc. and thus will also profit from volume and price appreciation. Note that Homerun Resources Inc. pays Zimtu Capital Corp. to provide this report and other investor awareness services.