Disseminated on behalf of Commerce Resources Corp. and Zimtu Capital Corp.

A few days ago on March 24th, my top pick in the REE (“rare earth elements”) space, Commerce Resources Corp. (“CCE”), announced the extraordinary achievement at bench scale to reduce the consumption of key reagents in the flotation circuit by a staggering 80%.

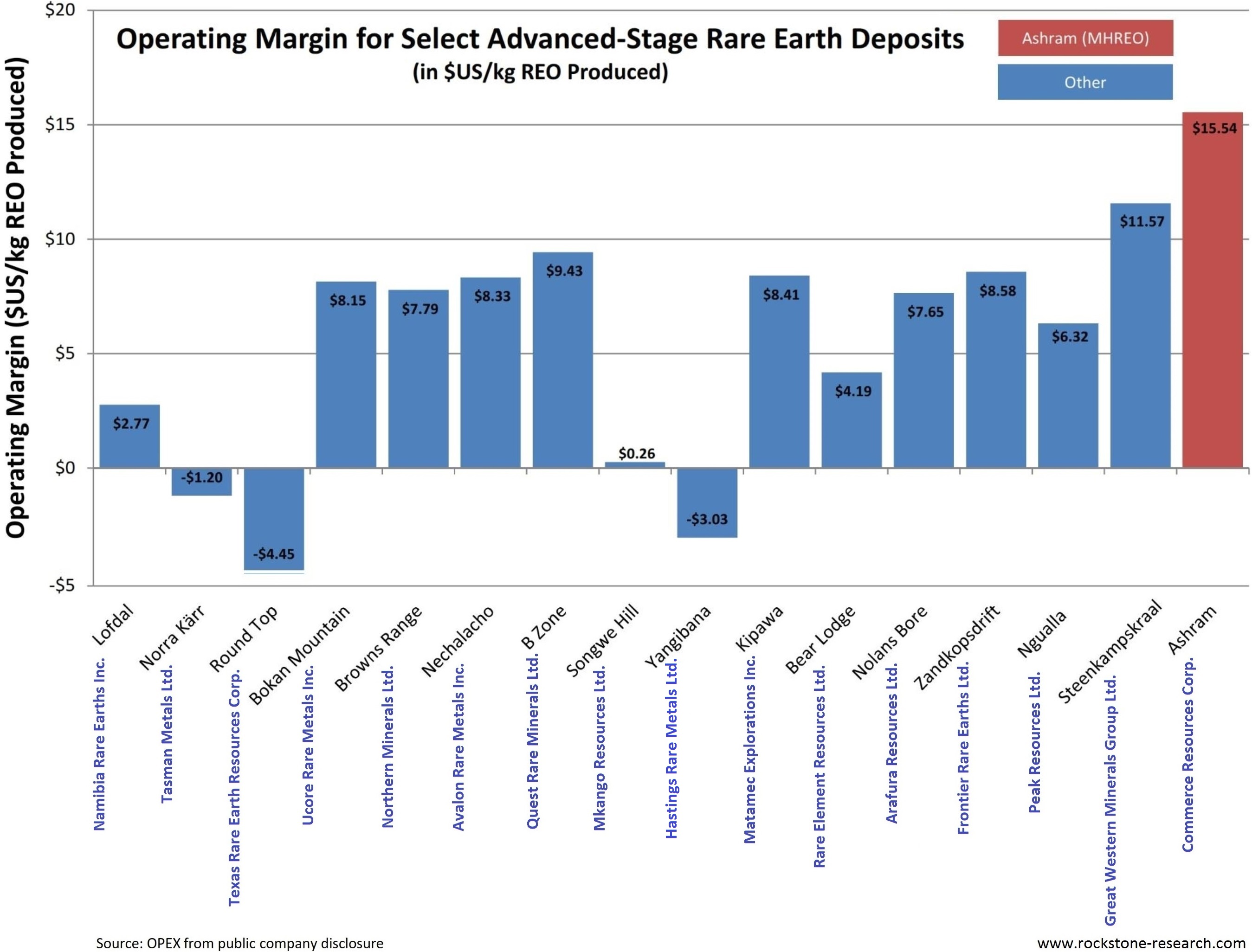

Prior to this considerable reduction, Commerce’s Ashram Deposit already had the highest projected operating margin ($15.54/kg REO produced, in USD) of all major REE development projects, as my last article “The REE Basket Price Deception and the Clarity of OPEX” illustrated. Further, that article detailed the following conclusion:

“The lower OPEX companies with good, balanced distributions will have the greatest chance of success in this complicated space. Using the current market basket price to approximate the operating margin, it is very clear that HREE enriched deposits (i.e. ones with higher basket prices) are prone to significantly higher OPEX, and significantly lower projected operating margins.”

I certainly take no pleasure in saying “I told you so”, but the REE space basically shrank by 2 companies on March 30th, within 8 minutes between news:

Great Western Minerals Group (GWG) is unable to restructure $90 million bond:

GWGÂ’s share price crashed by 75% to $0.01.

Strategic review of Frontier Rare EarthsÂ’s activities:

“This review is expected to be concluded in Q2 2015, after publication of the PFS Report. In the absence of a marked improvement in the rare earths sector, junior mining sector and overall equity capital markets in the coming months, it is considered likely that the Board of Frontier will recommend to shareholders that a new strategic direction be pursued with the objective of maximising the value of the Company’s assets for shareholders.”

It seems likely to me that FrontierÂ’s PFS wonÂ’t turn out too well, but at least management seems to be warning shareholders early.

Considering the most recent bad to extremely bad economic news for both Western REE producers (loss of $79 million USD for Lynas Corporation Ltd. and loss of $330 million USD for Molycorp Inc.), one does wonder what this space will look like in the future, if prices do not rebound significantly. However, I did take pleasure to talk with Professional Geologist Darren L. Smith (Project Manager of the Ashram Deposit) of Dahrouge Geological Consulting Ltd., as well as Chris Grove, President of Commerce Resources. Both also answered some questions from readers of my newsletter.

Interview with Darren L. Smith (M.Sc., P. Geol.)

Mr. Darren L. Smith is a Professional Geologist and graduate of the Carleton University with a Bachelor and MasterÂ’s Degree in Science (Geology). As a Senior Geologist/Manager with Dahrouge Geological Consulting Ltd., he is endowed with over 8 yearsÂ’ experience

in the mineral exploration industry, including over 6 years focused almost exclusively on rare earth elements (REEs). His experience includes carbonatite complexes and associated rare metals, REEs, and unconformity-associated uranium deposits. DarrenÂ’s primary role with Dahrouge is high-level project management with notable recent success through the discovery and advancement of CommerceÂ’s Ashram Rare Earth Deposit in northern Quebec. Darren led the exploration program that resulted in the discovery of the Ashram Deposit in 2009, and he has been instrumental in its advancement since this time. As Ashram Project Manager, Darren has provided technical oversight for preliminary economic assessments and prefeasibility-study-level project advancement, has set up and monitored complex metallurgical programs, and directs all field operations and development programs, as well as the projectÂ’s overall management.

Rockstone:

Considering Commerce Resources Corp.Â’s latest news of March 24th, the company achieved (at bench scale) a reduction in consumption of 3 key reagents in the flotation circuit by a staggering 80%. Can you please explain how this was achieved without losing flotation performance, why this is significant and what impact this will have for the upcoming PFS.

Darren L. Smith:

Developing a flotation scheme is an educated exercise of trial and error. There are many factors that have a material influence on flotation behaviour and performance and these would include pH, pulp density, temperature, retention time, air flow rate, agitation, reagent dosages and their ratios, and even the order the reagents are added in the test.

In this test, we simply reduced the dosage of the two carbonate depressants as well as the pH modifier while leaving the collector dosage unchanged. This effectively modified the ratios of the reagents and was coupled with a slight adjustment to the conditioning time and pulp density.

The benefit to the PFS will be positive through a more economic and optimized flotation circuit – and I mean lower costs. I cannot disclose any internal OPEX numbers we are projecting, but I can say that the lower reagent consumption has a considerable and positive impact on the economics of the flotation circuit. Lower reagent consumption also has a compounding benefit through lower costs of acquisition, and lower shipping-storage-handling fees. This is why we have targeted a decrease in reagent consumptions for ongoing optimization work.

Further, we have actually developed two competing flotation schemes, for the same rougher-scavenger flotation circuit, that use different reagents and dosages. Performance is very good with both schemes. We have also developed a flotation circuit that would depress the fluorite in addition to the carbonate, thereby increasing the grade significantly without the need of magnetic separation to remove this fluorite. We can achieve a >40% TREO mineral concentrate with this circuit; however, our recoveries are less than 55% at this time so some more work would be required. This is why we are currently focused on the circuit that leads to >40% TREO mineral concentrates at >70% recovery. This circuit also gives us a high-grade fluorite concentrate, at no added processing cost, that has by-product potential. All of this goes to highlighting the versatility in processing the Ashram Deposit material, with considerable room for improvement remaining.

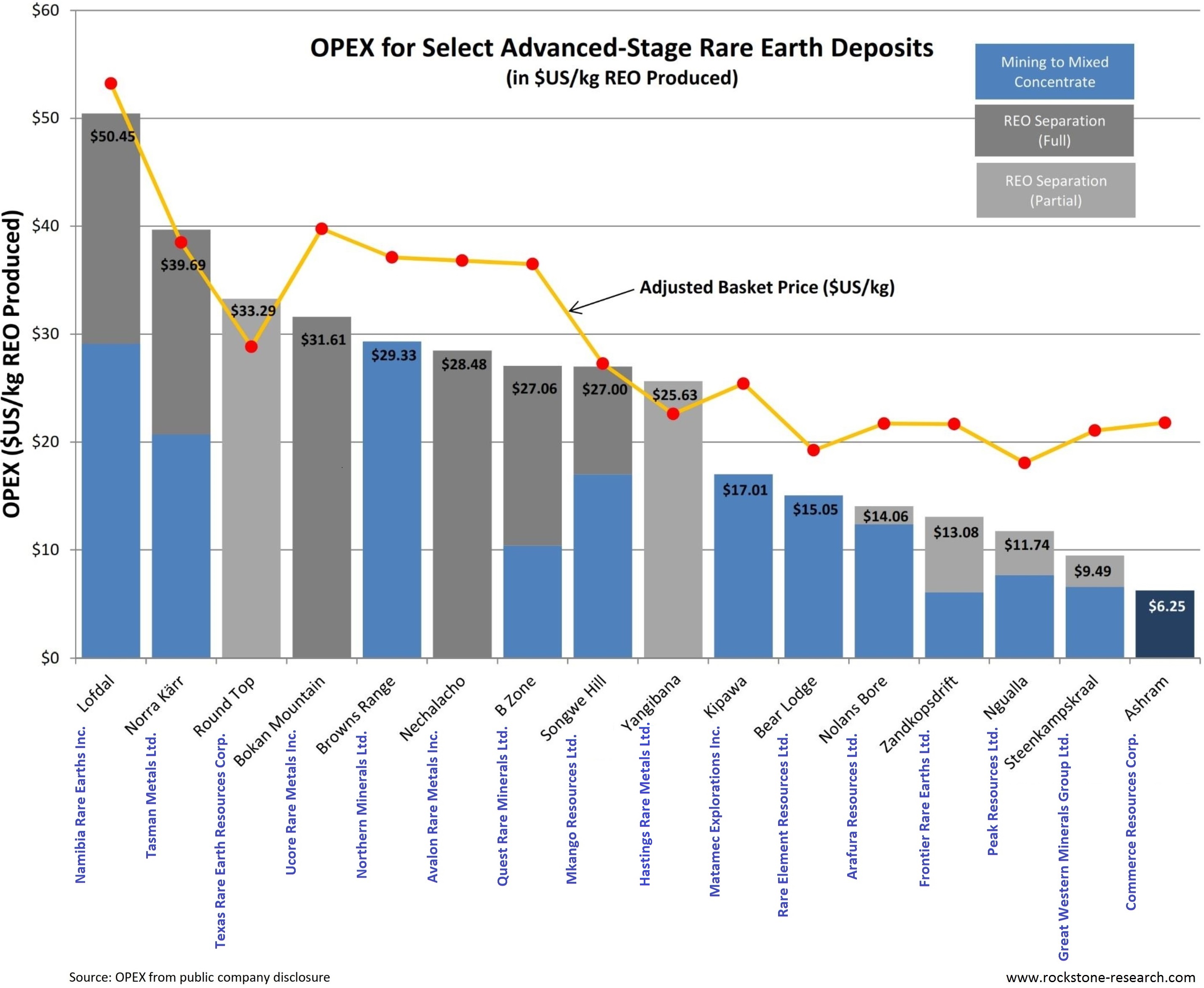

In the last Rockstone article “The REE Basket Price Deception and the Clarity of OPEX”, it was shown that Ashram has, by far, the lowest OPEX ($6.25/kg REO produced) of all major REE development projects. Can you say something about this number?

The numbers appear correct and, as in any commodity, the producers with the lowest costs and the highest operating margins will be the projects that are able to advance. These numbers for Commerce are not something that are completely unusual – they are arguably comparable to other projects that are also hosted by the three minerals (monazite, bastnaesite, and xenotime) that the Ashram Deposit is, and that currently enjoy commercial production. This is something that we have said for years is vitally important to understand – in other words, it is what minerals the REE deposit is hosted by that determines the project‘s economics to an overwhelming degree.

The data for these charts was sourced from company public disclosure ?noted in USD, AUD, or CAD. Given the varied currencies, and that the market basket price is noted in USD, the data was normalized to USD. An exchange rate of 0.78 and 0.79 was used to convert AUD and CAD, respectively, to USD. If not, we would be comparing apples to oranges. The exchange rate basically reflects how it is more expensive to build a mine in the USA, compared to building the same mine in Australia or Canada.

Currency exchange is something not often taken note of in the space. For example, many companies present their CAPEX in USD, however some companies present it in their native currency. A prime example is Commerce ResourcesÂ’ Ashram Project with a CAPEX of $763 M in CAD, which today equates to roughly $603 M USD, and well under $600 M USD if sustaining capital is not included. However, I consistently see the CAD value assumed to be USD and compared to USD in the market, which is very misleading.

Some people argue that Commerce may become a buy in Q3/4 2015, respectively when the pilot plant has produced some kg of representative REO. What do you think of that?

?Commerce is demonstrating their entire flowsheet using only standard commercial technologies to ?produce its end-products (mixed rare earth concentrates), and is starting with an ore that is hosted by REE minerals that dominate commercial production globally, past and current?.

This gives the flowsheet an inherent ‘derisking’ above many of its peers whom may be saddled with unknown and difficult mineralogy that may have forced a redirection of focus to new technologies that may work, but that may take decades to commercialize, if ever.

Very few companies have actually demonstrated their flowsheet through to their end-product with a viable low-cost flowsheet that utilizes commercial technologies. Many have chosen to skip over the front-end development and have jumped to targeting the generation of a product with no regard for recovery or economics of the process. Alternatively, Commerce chose to defer this more promotional route and to focus on developing a low-cost and practical flowsheet through to end-products (front-end and back-end) so they can stand behind the viability of the process.

In short, itÂ’s not a matter if CCE will generate its targeted end-product, itÂ’s a matter of when. Commerce is not just targeting the production of a mixed rare earth concentrate, they are targeting a mixed rare earth concentrate with a viable, low-cost flowsheet that uses only commercial processes.

I do not know if the dominant opinion is that the market will move the stock price positively on the announcement that this process has been completed. Please note, I am not an investment advisor but rather a humble geologist who enjoys investing in the market. Please consult a professional investment advisor who may be able to answer such questions.

What can we expect from CCE in the upcoming months in terms of newsflow?

Commerce raised significant capital in 2014 ($11.1 M) and ?will be focusing this capital into the ground at Ashram and in metallurgy to demonstrate the entire flowsheet. This will generate extensive news flow throughout the year as the project is advanced and further derisked.

Therefore, news flow will be regular and material as the field and metallurgical programs advance through the spring and summer. The sample analysis for the first drill holes should be received shortly with the flotation piloting nearly complete and HCl leach pilot ready to go.

Is there any interest from a potential strategic partner at all? What are they waiting for? Are they waiting for an REO sample from the pilot plant? People argue that a partnership may only become closer when the pilot plant is ready.

Yes, there continues to be significant interest. Commerce has been in discussion with several potential partners this past year with trips to France and Japan completed recently to further those discussions. We have at least four parties currently requesting a mixed rare earth concentrate to evaluate, including several with excess separation capacity, where our REO distribution would fit very well. I would also like to note that the samples we will be producing will be tailored to the specific SX (solvent extraction) facilitiesÂ’ feedstock specifications.

Do you think that REE prices will rebound again? If yes, why and when? How would things change for CCE finding a partner if prices were up again?

Yes, I do. In fact, very recently and for the first time in 4 years we saw a material price increase for two heavy REE’s – terbium and dysprosium – and a modest price increase for neodymium, a light REE. All three of these REE’s are essential for magnet manufacturing and Commerce Resources has good enrichment of them all. In general, higher prices will potentially be a trigger to the entire market that demand is exceeding supply and that it is time to make sure that any REE users have access to future supply. As such, the general lackadaisical attitude on supply may disappear overnight and buyers of the REE’s may again feel the need to look seriously at a joint venture or an off take agreement.

Overall, it has been argued – and I would agree with this – that China will be looking for higher prices through the two-step programs of President Xi. The first step, which is very public, is consolidating the state sanctioned REE producers into a half dozen REE conglomerates. This has been stated at least twice in news releases. The second step will most likely not be reported on per se, but it is potentially more significant and this is President Xi’s work to shut down the Chinese REE black market which has continued to have a negative impact on REE prices overall. So, I expect to see tighter supplies and more upward price pressure for the future. Additionally, it has been said that the biggest buyers of the Chinese black market are the Japanese and the Koreans, and so if this supply stream is affected negatively, you would assume this would then affect these countries significantly.

“Quebec is re-establishing itself as one of Canada’s – and one of the world’s – most attractive jurisdictions for mining investment, according to an annual global survey of mining executives released today by the Fraser Institute, an independent, non-partisan Canadian policy think-tank. ”Quebec was atop the national and international rankings from 2007 to 2010 but tumbled down the list in recent years as a result of increased red tape, royalty hikes and uncertainty around new regulations,” said Kenneth Green, Fraser Institute senior director of energy and natural resources. “The confidence mining executives now have in Quebec is due in part to the province’s proactive approach to mining policy and its Plan Nord strategy to encourage investment and mineral exploration in northern Quebec.”

A “hurdle” Ashram seems to face is its remote location and lack of infrastructure. Is that the main reason why no strategic partner has been found yet? How are things developing in that respect in Quebec?

The project is relatively remote; however, this hurdle is all too often exaggerated and I would argue that this is not considered a significant issue by the parties interested in the project at this time. The Ragland Mine has successfully operated in the area since the mid-90s and it faced similar logistical challenges in the beginning for example.

The Ashram Project is located in Northern QC, about 130 km south of Kuujjuaq which is serviced daily with non-stop flights from-to Montreal. There is also air service from-to nearby communities, as well as several sealifts in the summer for bulk shipment of materials. This makes Kuujjuaq a very good staging area for the project, complete with all air charter services including float/ski equipped fixed wing aircraft and a helicopter base.

The project requires ~180 km road to the coast which has now been derisked to a high level, and is projected to cost less per km to build than was outlined in the PEA. It runs north-south, and therefore, along trend of the geology making it less technically challenging than if built east-west. It has only three water crossings and does not cross any critical hydrology, flora, or fauna habitats. There is the upfront capital cost to build; however, this is also offset by the low-cost mining and low-cost metallurgy. The volumes shipped are also relatively low for a mine of this nature, meaning only a low-cost barge facility is required for loading on seafaring vessels, and the constrained shipping season of 5-6 months is not of large concern.

Further, the QC Government continues to position itself for advancing infrastructure in the region, and although this is not likely to be in place prior to Ashram production, there is likely to be significant positive impact in terms of transportation and power for the project when it does occur.

The following questions are from some of the Rockstone newsletter readers:

Do you think the best time to buy CCE is now, or when the pilot plant is operational, or when the PFS is completed, or when a strategic partner has been found?

I am not an investment advisor and so it is inappropriate for me to answer this question. However, each of these three aforementioned events, if successful, are milestones that move the project materially forward. I would anticipate a positive market reaction at each announced success.

CCEs host mineral is monazite, which can be separated by RhodiaÂ’s plant in La Rochelle. Eudialyte from Tasman Metals is exotic; to separate rare earth oxides will not be easy. In order to separate eudialyte, would Rhodia need to buy different machines for eudialyte separation, or could they use the existing ones, or would they have to build a whole new separation plant just for eudialyte separation? Any idea how much this would cost? It seems to me that Rhodia has no huge extra costs to separate CCEs host mineral monazite, correct?

There is a common point of confusion in the market on what a separation facility, like what Solvay runs at La Rochelle, processes as feedstock. Rare earth separation facilities do not separate minerals; they separate mixed rare earth concentrates, typically as a rare earth oxide (REO), rare earth chloride (RECl), or, as in the case of La Rochelle, a rare earth carbonate (REC). Each separation facility will accept only a certain type(s) of feedstock to process, such as per above, as well as a limited range of REO distribution based on their separation circuit set-up.

Most world facilities are LREE separation facilities and therefore cater to LREE enriched feedstock. Some facilities, such as those that cater to the South China Clays, may accept an HREE enriched feedstock. It is a CAPEX intensive and complicated venture for a separation facility to modify the type of and REO distribution of its feedstock, and is why they look for long term and stable sources of the proper feedstock for their specific facility. This is something that the Ashram Deposit has in spades – a huge resource of consistent feedstock.

Therefore, from a market investing perspective, I suggest there are two things an investor should note in this regard. Firstly, how amenable is a host deposits mineralogy to low-cost and viable metallurgy through to a mixed rare earth concentrate (REO, RECl, REC) (i.e. can they economically produce a mixed concentrate), and second, what will that mixed rare earth concentrateÂ’s REO distribution be?

In short, La Rochelle, and most other rare earth separation facilities would have little trouble processing the concentrate from the Ashram.

Alternatively, as eudialyte has never been commercially processed and its rare earth distribution is quite unique in the rare earth space, it may be very difficult to find an existing facility that could accommodate its processing.

Will the pilot plant also test material from the bulk sample of Upper Fir?

No. The current flowsheet demonstration is focused on Ashram only at this time. However, we are planning a pilot demonstration for the Upper Fir Project, as the deposit also boasts very favourable metallurgy, through to the production of 99.9% technical grade tantalum and niobium oxides.

Anything new on the Southeast Area of Eldor?

We are very excited about the niobium potential at Eldor and are close to honing in on a high-priority drill target in the Miranna Area, just north of the Southeast Area. One week of prospecting is scheduled for this summer to locate the source of a boulder field and spot final drill holes. As Ashram remains the focus of expenditures on the Property, it is not clear if a drill budget will be allotted for any niobium targets this year.

In short, there is significant potential for a sizable, high-grade niobium deposit in the Southeast and Miranna areas based on numerous >10% Nb2O5 boulder samples in the area as well as mineralization already encountered in drill holes.

It is likely any niobium would be accompanied by significant tantalum, phosphate, and also a heavy rare earth enrichment that may be recoverable with the niobium.

How many kg of mixed oxide will eventually be produced by the mini pilot plant? Will those kg be sent only to Solvay? Or are more (2-3?) interested to look at the result?

The target is 3.0 kg of Ce-La depleted mixed REC and 0.5 kg of mixed RECl that will meet the impurity tolerances of global separation facilities. We have enough material on hand to generate much more if needed. Yes, we have four parties with formal requests for material, including Solvay.

TMR from Gareth Hatch “will also look at the development and validation of computer simulation tools, for the accurate modeling and rapid optimization of existing and new REE separation processes.” Does Commerce give them, and thus the US Department of Defense, a feedstock sample from Ashram?

We have not provided feed for this work yet, as they required a large volume of a mixed rare earth concentrate to begin with, I believe.

However, we have had discussions with Gareth regarding this work and look forward to hearing more about the process as it continues to be developed.

What will happen to the fluorite in respect to the pilot plant? Will it be extracted as well in order to show it to someone for analysis?

Yes, the fluorite produced will be evaluated for its use in the fluorspar industry. It is literally the tailings from the WHIMS process, with the concentrate being the final rare earth mineral concentrate.

If proven to fit the criteria for met-spar, this would be a significant development for the PFS over the PEA through another cash flow stream with zero added processing cost, and also for the fluorspar industry as few of those types of mines have such long mine-life potential.

What’s the approximate time span after handover of the sample to an interested party until they know “if it works”?

ItÂ’s not so much to know if it works, but rather to confirm it is what you say it is. This is something on the order of weeks to a few months perhaps.

They will confirm its distribution and that it meets all its feedstock specifications. At this point they would request more material for bench scale work and we are positioning ourselves to quickly be able to provide this. It has already been inferred a second sample is likely to be requested by some parties.

With the proper funding, when could CommerceÂ’s Ashram be in production? What is the most optimistic timeline?

End of 2018, early 2019.

Interview with Chris Grove (President of CCE)

Mr. Chris Grove was involved in the seed financing round for Commerce Resources Corp. in 1999 and began working for the company in 2004 in the Investor Relations department. He was instrumental in liaising with institutional investors in North America and Europe for financings for the company since 2005, raising over $70 Million for the company. Mr. Grove was added to the Board of directors in 2012 and in September 2014, was appointed as President of the company. “This realignment of executive positions is to advance the corporate focus of development through a partnership arrangement.” said Dave Hodge, former President, who continues as CEO and Director.

The following questions are from some of the Rockstone newsletter readers:

How much money has been spent already for the PFS on Eldor and how much more is roughly needed to complete it?

Specifically we have spent about $9.0 M so far on the PFS for the Ashram. We expect that with programs totaling about $5 M we would be able to complete the PFS.

How does Commerce judge the nerves and patience of its shareholders? Is the stock slowly but surely going down and is it possible that larger shareholders are/will be selling more and the price will crash?

All of the management of CCE are also shareholders and we all frustrated by the market, which is the dominant factor affecting our share price. Remember that in March 2011 we were trading at $1.08 when the Venture Exchange was also at a high. Since that time all Venture listed stocks have corrected downwards.

However, the main differences between CCE and most companies is that in this 4 year period we have released PEAÂ’s on both of our assets, have continued to be able to access capital and have continued to advance both of our deposits, with the greatest amount of work being done on the Ashram.

As well, if you expand your time horizon slightly, you will see that for most of 2013 we were trading in the $0.06 range, and so where you decide to start your view of trading range is also important.

Why is Commerce not releasing more information of whatÂ’s happening in the background? Does an offer exist for the whole of Commerce, or parts of it, for a sales price that is lower than management was hoping for? To put it differently: What is Commerce actually waiting for right now and why is Commerce sticking to its way? What makes you think that the stock will go up again?

As a public company, the rules governing news dissemination is such that you should have something to release that is of “material interest” to the company and or its’ projects. Reporting on such activities as trade shows, corporate development meetings, etc, is not generally done unless there is something specific that has been accomplished. The achievement of significant milestones and the ongoing work for the Ashram should be recognized by the market at some point.

There exist 2 PEAs – one for each project. If you could please roughly calculate with the new/changed parameters, how would the PEAs look today (e.g. NPV)?

This is the objective of a PFS – to calculate to a higher degree of accuracy than what was detailed in the PEA’s for both projects. The 43-101 legislation requirements are such that we do not disclose this information prior, even if we have generated it internally.

One answer in terms of how different would the specifics for each project look today as opposed to the same specifics as they were detailed in the released PEAÂ’s, is to say that we are working towards improvements to be made for both projects.

How is it going with Deloitte? Are they actually still working for Commerce?

Deloitte is still working for Commerce Resources (since November 2014) and they are doing an excellent job of identifying and contacting potential joint venture partners on our behalf. When we first engaged Deloitte (February 2012 through to January 2013) we had meetings with essentially all of the major players in the REEÂ’s in China, and all of the major buyers of the REEÂ’s in Japan and Korea. However, in a market with sharply falling REE prices (2011 through to 2014) and in consideration of the incoming and reform minded Chinese President Xi, it was a surprise to all as to how no corporate development was achieved by anyone. This time around we hope that the result is profoundly different.

Please explain how a potential partnership would look like as per CommerceÂ’s plans (agreement wise).

Our intent is to secure a project level investment, such as either an off take agreement or a percentage sale of the asset. As such, both styles of investment would not typically involve new equity but would instead be capital from the joint venture partner for either a percentage of our future production (off take) or a percentage of the actual asset. In terms of these two different styles of project financings I would direct you to the deals between Mitsubishi and Copper Mountain, and then between Fortune Minerals and Posco. It would be our goal, with the capital invested, to complete our Bankable Feasibility studies for both projects.

When do you think Commerce will secure a strategic partnership: before the pilot plant is operational, or thereafter, or when the PFS is completed?

Part of the conversation with potential partners is an invitation to be involved at this stage of development, while we are still determining key elements of our flow sheet and exactly which products to be produced. Therefore, it is suggested early involvement with the company should be attractive to these potential jv partners. It is like the story of the “Little Red Hen”; the earlier you are involved, the more say you will have in the project and the bigger share of the bread you will get.

Other REE developing companies signed offtake agreements during the last years, why did CCE did not sign any? Why is CCE not going the same route?

Commerce is not in a rush to sign an MOU that has no substance or tangible benefit to the company even though a short, temporary stock lift may follow. We have been approached and have had many discussions and continue to work towards an agreement that would advance the Ashram Project with a tangible investment. An offtake agreement, for example, has little benefit to a junior unless capital is involved or unless it is part of a larger strategic business integration; without the commitment of capital it does nothing to advance the company to production.

You have mentioned offtake agreements with other companies, but as far as I know, none of these have publically declared a commitment of capital from the major to the junior.

About MolycorpÂ’s Mountain Pass Mine and SilmetÂ’s separation plant: Are they able to separate AshramÂ’s feedstock without huge investments? Would the Silmet plant be capable to separate Upper FirÂ’s tantalum and niobium ore? Could CommerceÂ’s both metallurgies be easily integrated into MolyÂ’s business?

Our feedstock is likely to be a very good fit for MCP; however, we are about 8 times more enriched in the HREEs by comparison so I am not sure how this would impact their current set-up at Mountain Pass for example.

Molycorp’s Silmet plant in Estonia is set up to process both loparite hosted material from the Lovozero Mine in Russia – the only loparite hosted deposit mined and processed globally (as far as I know) – and also pyrochlore hosted tantalum and niobium concentrates very similar to what the Upper Fir has.

So, yes Silmet could process the ore from the Upper Fir, but Silmet is not set up to process the three REE bearing minerals that the Ashram is hosted by, at this time.

However, as is common in the tantalum and niobium world, it would be essentially impossible for Commerce Resources to be paid by Silmet Molycorp for both metals – the presence of a by-product, or a co-product is not something that is accommodated by anyone in the tantalum and niobium world and that is why the business plan for Commerce Resources is to process our ore all the way through to separated oxides on site in British Columbia, and then to ship anywhere in the world, 99.9% pure tantalum and niobium oxides. The current market for niobium is good and the market for tantalum is arguably in a significant shortfall position.

Thanks for the interview. I wish you success while I am looking forward to it.

Disclaimer: The author, Stephan Bogner (Dipl. Kfm., FH), owns shares of Commerce Resources Corp. and thus would profit from a share price appreciation, whereas the author may sell those any time without notice. Neither Rockstone Research nor the author was remunerated or instructed by Commerce Resources Corp. to produce or publish this content. However, please read the full disclaimer within the full research report (available as a PDF below) as a conflict of interest exists with Zimtu Capital Corp. and none of this content is to be construed as a "financial analysis" or "investment advice".